Mornings on Wall Street are quiet these days. Sputtering IPOs and a vibrant private market have made it less tempting than ever to ring the opening bell. With companies staying private for longer and raising plenty of private capital, this trend doesn’t show any signs of slowing down.Imagine you didn’t have to wait to go public (or get acquired) to turn stock options into cash. That’s where liquidity programs come in. Private companies are increasingly giving shareholders a chance to get real value from equity before an exit.

But some companies are still reluctant to embrace liquidity. Liquidity myths, particularly around employee retention and financials, have led some to hold back.

Carta recently hosted a panel on the subject of liquidity—and why it isn’t the boogeyman some businesses fear it is. The panel featured investor Elizabeth Weil, lawyer Michael Irvine, and Carta CFO Charly Kevers. Stanford professor David Larcker moderated the discussion.

Liquidity myth #1: Employees will leave

With little incentive to go public, businesses can’t use the promise of a lucrative exit to keep employee turnover in check. Ownership, a motivator for new hires and employees alike, loses its luster if it a payout appears far off. So, contrary to popular belief, offering liquidity actually encourages employees to stay put.

Without liquidity, “you’re basically forcing the employee to make a decision: ‘Am I going to stay or am I going to leave?’ And by actually allowing them to get some liquidity, we believe it’s going to help drive retention,” says Irvine.

Similarly, in a competitive job market, liquidity keeps outside callers at bay. Being able to cash in on equity when you’re short on funds or approaching a life event could dissuade employees from leaving for the highest bidder.

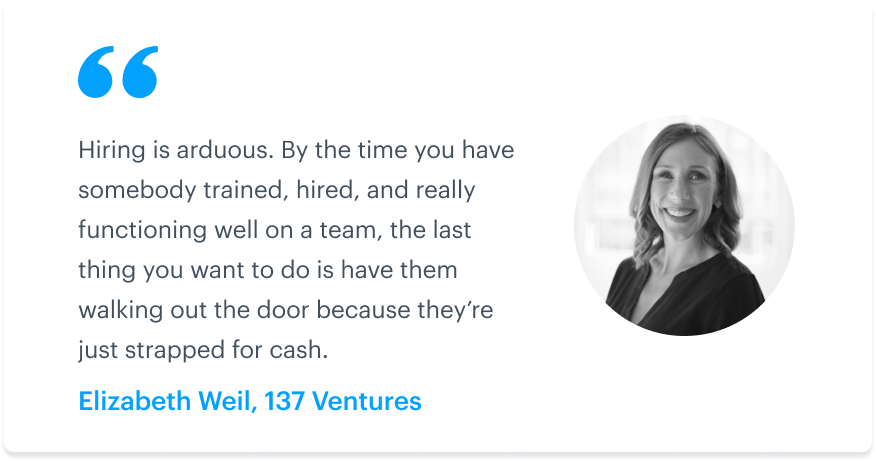

“Hiring is arduous. By the time you have somebody trained, hired, and really functioning well on a team, the last thing you want is to have them walking out the door because they’re just strapped for cash,” says Weil.

Liquidity myth #2: It’ll mess up our 409A

Companies offering equity need a new 409A valuation every year, which can affect the strike price of their options. Many companies worry that liquidity could rock the boat and dramatically increase their valuation. But that doesn’t have to be the case.

When handled carefully, liquidity events don’t have to be problematic for valuation. It’s all about structure and what your company’s priorities are.

“There’s the impact on 409A, there’s the impact on taxes both for the company and employees, and also the issue of access. Think of it as a balancing act—you can’t get all three perfect,” says Kevers.

The impact on your 409A depends on a number of factors, including frequency, scale, and access. Every case is different—it’s all about how you structure your liquidity program. Are all employees allowed to participate immediately, or is access based on tenure? If you’re not running a formal tender offer, what are the participation criteria?

Making that call is a difficult one, and when not handled well, it can create a culture of “haves and have-nots,” as Weil put it. But when you’ve mastered the balancing act, with the help of accountants and your CFO, you can offer up liquidity in a controlled manner that entices newer hires to stay and doesn’t wreak havoc on your 409A.

Liquidity myth #3: Our investors won’t like it

No one wants to upset the board or investors. For some, the notion of giving employees the right to sell pre-IPO seems radical. But it really isn’t.

“Companies have to do this to attract the right talent. Investors will have to accept that in order to attract talent that drives value, they’ll have to be okay with it,” says Kevers. Investors today aren’t naive or skittish about liquidity’s value as a retention tool.

There are also more immediate, tangible reasons for investors to support liquidity programs.

As companies issue stock to employees and new investors, everyone’s respective percentage of the pie shrinks from dilution. Investors, looking to maximize their return or maintain ownership targets in a company, are never thrilled to see their overall share of the cap table shrink.

Liquidity events are great for offsetting dilution. Shareholders—including investors—get a chance to turn some of their shares into cash, while existing investors have the opportunity to buy more of the company. If investors choose to sell some of their stake during a liquidity event, they get the chance to show real results to their limited partners a little sooner.

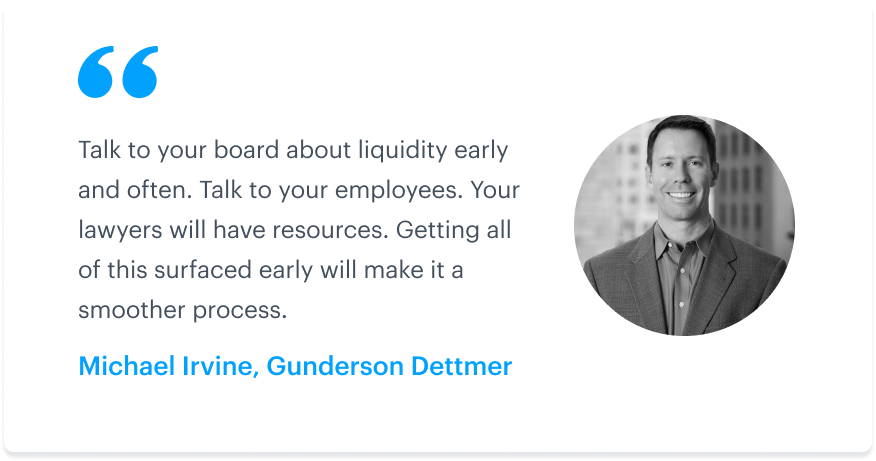

“Talk to your board about liquidity early and often. Talk to your employees. Your lawyers will have resources. Getting all of this surfaced early will make it a smoother process,” says Irvine.

Similar to how offering equity became a Silicon Valley expectation in the late nineties, liquidity is already on course to becoming a table stakes offering—or even a shareholder right. “Maybe a third of the companies in the valley allow some form of sale at this point,” says Larker.

Fear of the unknown might hold some back. But with average tenures falling and tech IPOs taking longer than ever, companies that don’t offer liquidity could be risking something far worse than the boardroom’s ire: losing talent and falling behind.