For many founders and startups, closing a round of seed funding is a landmark event. A seed deal is often the first time a company raises money from venture capital firms or other institutional investors. Seed funding is a sign of validation from VCs that a young startup is on the right track—and it may be the beginning of a fundraising journey that will include more venture capital to come.

At every other stage of the startup lifecycle, 2023 has already brought significant movement— both upward and downward—in the market for venture-backed round sizes and valuations. But at seed, which is typically home to the most quarterly investments on Carta of any stage, the status quo remains largely intact.

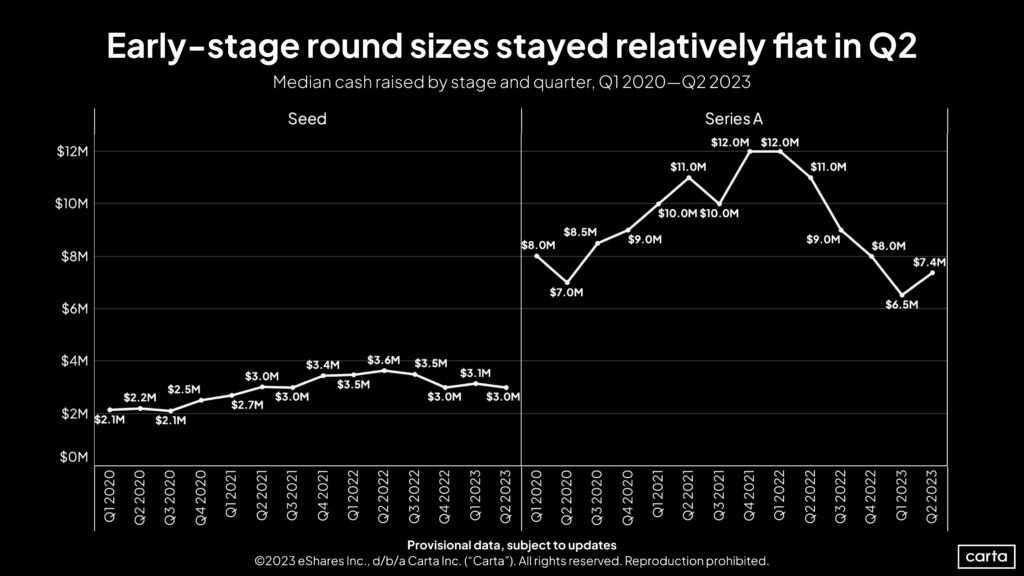

Initial data from the second quarter shows that the median seed deal on Carta was $3 million in Q2, down slightly from $3.1 million in Q1 and equaling a $3 million median from Q4 2022. That’s a 3% quarter-over-quarter decline in Q2 following a 3% increase in Q1.

That’s much less volatility than at other stages, such as Series A, where the median round increased by 14% in Q2 after declining by 19% in Q1.

While the recent variance in the size of seed rounds has been slight, the minimal movement has not been in line with trends at other stages. The median seed deal inched up in Q1, then decreased in Q2. The opposite was true at each of Series A, Series B, and Series C: The median deal at those stages got smaller in Q1, then increased substantially in Q2.

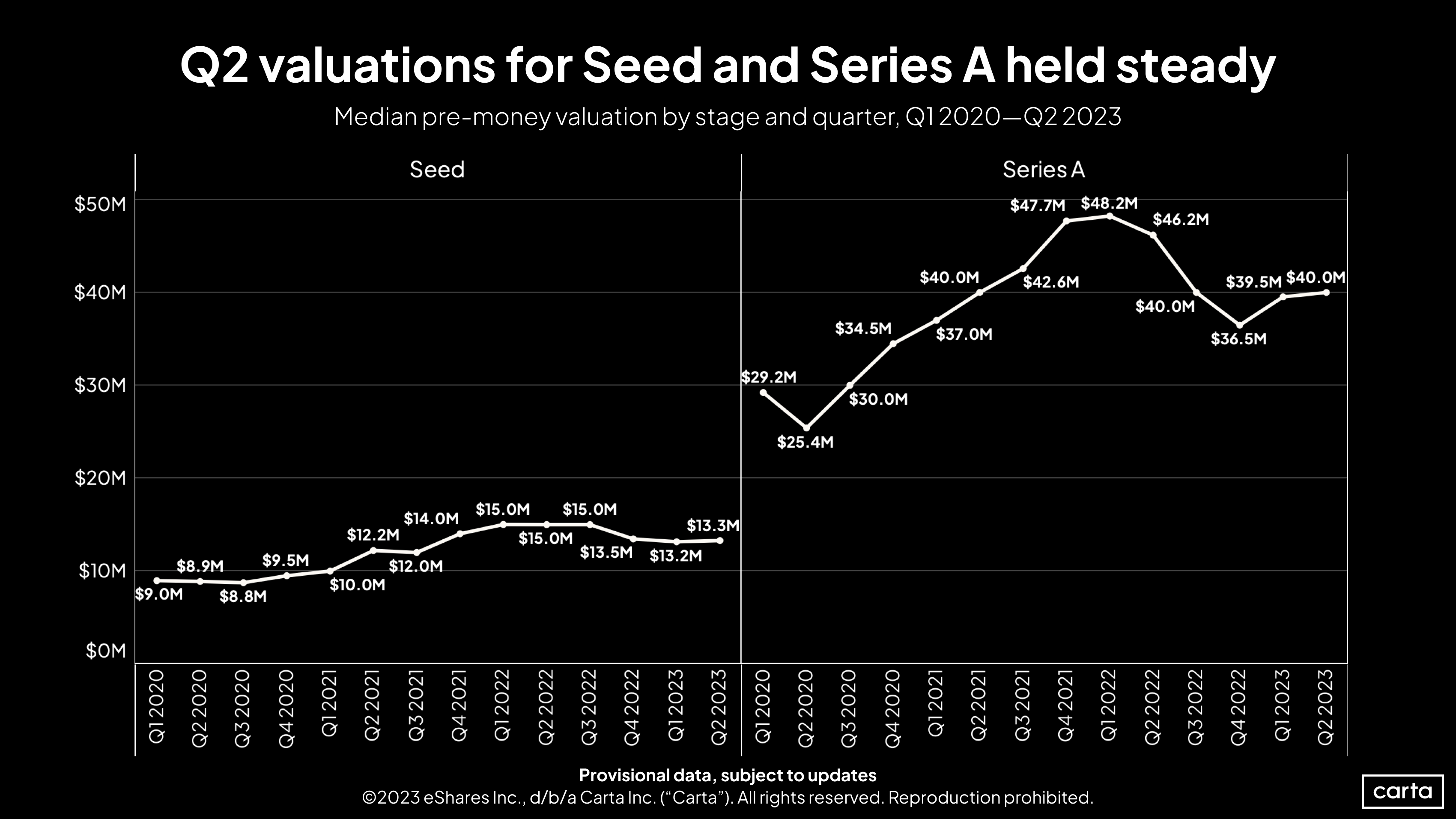

The seed stage is also staying level in terms of valuations. The median seed valuation on Carta was $13.3 million in Q2, up less than 1% from Q1, when the median was $13.2 million. That figure was down from $13.5 million in Q4 2022, a decline of about 2%.

Again, other stages have felt more turbulence. Series A isn’t too far off, with an 8% increase in Q1 followed by a scant 1% uptick in Q2. For late-stage startups at Series E and beyond, the median valuation fell by 60% in Q1, then recovered with a 105% leap in Q2.

Why seed is holding strong

The past few years have been a volatile time for venture capital. There are exceptions, but in general, the volatility has been more pronounced the later you go in the startup lifecycle. That trend continued in Q2.

The median seed deal increased by 67% between Q1 2020 and its recent high point of $15 million, which it first reached in Q1 2022. Since that peak, when the market has entered a slowdown, the median seed valuation fell by a maximum of 12%.

At Series B, the median deal size increased by 85% from Q1 2020 to its bull-market peak, then declined by 50% during the downturn. At Series C, deal size grew by 171%, then fell by 58%. At Series E+, deal size grew by 225%, then fell by 86%.

This difference in volatility across stages is largely a function of different timelines in the startup lifecycle. Older startups tend to be closer to an exit, either through an IPO or acquisition. Thus, investors tend to compare late-stage private valuations closely to valuation trends among public companies—the ranks of which those late-stage startups hope to soon join. Fundraising at the seed stage is more insulated from wild public-market swings like those we’ve seen in the past few years. That’s because those early-stage startups are likely still quite far from a potential exit.

Seed founders have certainly had to adapt to changes in the startup landscape over recent quarters and years. But so far in 2023, seed round sizes and valuations have been two uncommon areas of consistency.

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.